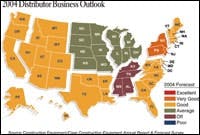

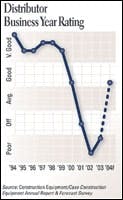

A Solid Rebound

Distributors reported the third straight year of sub-par business, chalking up 2003 as "poor," just slightly below the "off" in late 2002. Projections for 2004, however, are up to "good," which is a solid rebound from the slide and would match the rating of 2000.

This year, we teamed with the Associated Equipment Distributors to survey only their members, but historical trends/comparisons will still be valid.

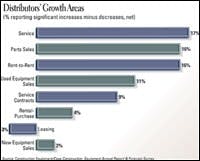

Sales volume increased for 25 percent of distributors, but were offset by volume decreases of 20 percent for a net of 5, albeit a positive showing. For 2004, 46 percent of distributors expect volume growth with only 3 percent anticipating a decrease for a net of 43.

Significant increases in volume were reported in service, with 29 percent seeing increases minus 12 percent citing decreases for a net of 17; parts and rent-to-rent showed a positive net of 16. Used-equipment sales showed a net of 11, and new-equipment sales were stagnant.

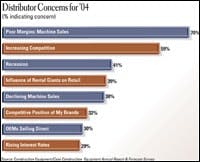

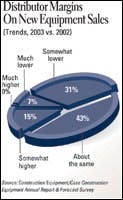

New-equipment margins were steady for about half of distributors, and the percent noting increases doubled over 2003. Yet, that percent still was less than the percentage citing margin decreases, leaving distributors with a negative net of 23.

Poor sales margins and increasing competition among distributors ranked No. 1 and 2 as business concerns. Eighty-eight percent said the market was intensely competitive or very competitive in terms of pricing, model selection and number of brands available. In the Mountain region, that number rose to 94 percent. It was also highest among heavy-equipment distributors, also 94 percent.