Setting the internal charge-out rate is probably the most difficult, contentious and important task that an equipment manager needs to perform. Let’s look at each of those words to better understand the situation and then attempt to develop a process that helps.

Difficult

The difficulty in setting a good, accurate internal charge-out rate does not come from the complexity of the calculation. Simple, straightforward calculations often yield the best results, and nothing is achieved by making things more complicated than they need to be. The difficulty comes from the fact that rates are estimates of future costs that are uncertain and in many cases unknown. Some, such as a known or quoted purchase price or lease payment, are well known; others such as annual utilization and future repair costs, can vary across a wide spectrum.

Accuracy in an estimated rate does not come from the complexity of the method you use to perform the calculation, it comes from the quality and the stability of the data you have available to perform the calculation. Focus on collecting good data and analyzing them in a simple, straightforward, well-understood manner.

Contentious

The rates will be used to develop internal equipment charges against the sites and internal equipment budgets or cost recoveries within the equipment account. Folk responsible for performance at a site level will want to be charged as little as possible. Folk responsible for balancing the equipment account will want to generate as much “revenue” as possible. Personalities, gamesmanship, one-upmanship, and our drive to produce the best results possible within our responsibility center all come into play.

The truth is, internal rates and charges “cancel out” when determining company performance and they affect alignment and motivation more than they affect business performance. Rates that are seen to be unnecessarily high or arbitrarily set will cause sites to take all sorts of retaliatory actions. Rates that are too low and make it impossible to balance the equipment account will provide neither motivation nor incentive within the equipment group.

As with most things of this nature, the answer lies in transparency and communication. Make sure everybody knows what is included in the rate and what is not part of the rate. Make sure everybody knows how the rate is calculated and how the whole internal charge-out process works.

Important

Reliable and competently set equipment rates are extremely important to almost every part of the company. They affect the whole of the job-costing system and all the processes used to measure, manage and improve crew performance on the job. They lie at the heart of the equipment-costing system and establish the baselines needed for the repair/rebuild/replace decision. They make fleet management and planning possible and, if properly structured, enable you to slice and dice the equipment account to produce the actionable information you need to analyze variances and get cost back on track.

It is not possible to overstate the importance of reliable and competently set equipment rates in the estimating process. You cannot estimate the cost of completing work if you are not able to estimate the cost of the resources used to produce the final product. Equipment rates are “estimates within the estimate,” and you simply cannot have confidence in a bid estimate if you do not have confidence in the equipment rates used to prepare that estimate.

A process

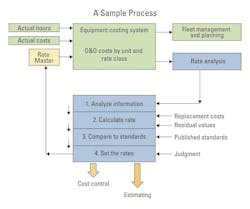

The importance of setting rates and the impact they have on many critical functions in the business means that you must have a structured process for assembling the required information and using it to achieve the best and most defendable results. Let’s look at the nearby flow chart and go through the steps needed to develop a process.

The green boxes show that it all starts with a good, solid equipment-costing system that collects actual hours worked and actual costs to determine owning and operating cost by unit and rate class. These costs are compared with budgets based on current rates to produce all the unit- and rate class-level information needed for fleet management and for making repair/rebuild/replace decisions. This is the normal or day-to-day use of the costing system, and it should be in place and working at most companies.

The blue boxes show how the same cost and budget information can form the starting point for the rate-analysis process. Clearly analyzing actual cost data and using the experience accumulated in the cost data base is step one in the rate-setting process. All available information must be reviewed, analyzed and, if necessary, adjusted to provide a solid starting point based on company experience. There is nothing wrong with eliminating some outliers, adjusting for old machines that will soon be retired, and doing everything you can to acknowledge the fact that historical information will be used to set rates for the future.

Step two in the process requires that you calculate an owning and operating cost rate from first principles using one of many available rate-calculation formats. Estimated replacement costs and residual values will be required inputs to the owning cost calculation, and substantial use will be made of historical data in estimating operating costs. The calculation should acknowledge the fact that owning and operating costs vary over the lifecycle of the machine and should seek to define both the magnitude and the timing of the “sweet spot” or economic life. The magnitude ($ per hour) of the sweet spot will be important in the rate-setting process: The timing of the sweet spot (hours worked) will be important in managing fleet average age.

Step three in the process requires a review of published and, perhaps, competitive rates. The Rental Rate Blue Book published by EquipmentWatch, the Ownership and Operating Expense Schedules published by the Army Corps of Engineers, and the many guides published by state departments of transportation are good examples of outside sources that can be used for comparative purposes. Be familiar with the rate calculation methodologies used and be sure that you are comparing apples with apples when it comes to defining differences between published standard rates and your internal charge-out rates.

The last of the blue boxes requires that the three sources of information—actual cost rates, calculated cost rates, and standard published cost rates—are brought together, reviewed and compared with existing rates as the final step in the rate-setting process. Judgment is shown as a necessary input. It is not going to be simple, there will be differences, and it will be necessary to calibrate and change rates to arrive at a final solution. Existing costs from box 1 will weigh heavily if they are solid and reliable. Calculated rates from box 2 will weigh heavily if good field experience is in short supply. Published standards will weigh heavily if these are seen to be applicable to the situation at hand.

Nevertheless, a decision must be made and a new estimated rate must be set. The new rates will update the equipment master used in the equipment-costing system. They will also be carried forward into the job-costing system and, most importantly, into the estimating system.

The last step—carrying the rates forward into the estimating system—is critical and is, indeed, the object of the exercise. Errors from incorrect rates in the equipment-costing system affect internal transfer charges. As such, they are important but not fatal. Errors from incorrect rates affect competitiveness and accuracy at the bid table and can be fatal. Set them too high, and you are unlikely to be low bidder. Set them too low, and you will be faced with a lot of unprofitable work.

Setting the “right” rate is probably your most difficult task. The future of your company depends on it.

About the Author

Mike Vorster

Mike Vorster is the David H. Burrows Professor Emeritus of Construction Engineering at Virginia Tech and is the author of “Construction Equipment Economics,” a handbook on the management of construction equipment fleets. Mike serves as a consultant in the area of fleet management and organizational development, and his column has been recognized for editorial excellence by the American Society of Business Publication Editors.

Read Mike’s asset management articles.