5 Steps to Accurate Hours Data

We constantly work to balance the cost of owning and operating our fleet with the revenue earned by charging jobs for the equipment they use. It occupies a large portion of every day. We worry about the cost side and struggle to bring it in line with our revenue so that we can “break even.” Yet we seem to worry less about the revenue side: How much do we charge for the hours, days or weeks worked by each and every unit in the fleet.

Managing cost is critical, and I do not want to underplay the importance of analyzing expenditure to make sure it is in line with what you expect. You need to understand the “DNA” of your costs (see “The DNA of Equipment Costs”) and know what is going on so that you can take appropriate action. The budgeting process does, however, rely on comparing cost with revenue and, if you want to balance your books, you need to get revenue right. It is just as important as cost and should not be taken for granted.

To get revenue right, you need to manage it with the same skill, care and attention as you use to manage cost. Many business systems, such as payroll, accounts payable and work orders, are in place to ensure that costs are correctly calculated and charged to units and categories. The question is: What procedures are in place to ensure that hours are correctly recorded and that the revenue is correctly calculated at a unit, category and fleet level? And, above all, do the revenue-collection procedures work reliably and efficiently?

Let’s go through the above diagram to understand the basics. I will then list five steps you can take to ensure that hours worked are properly recorded. We will end by briefly discussing the impact that inaccurately reported hours can have on other parts of the business. We will use hours, hours worked, and cost per hour as the basic unit, but clearly, everything we say applies to situations where utilization, cost and performance are measured on a daily, weekly or monthly basis.

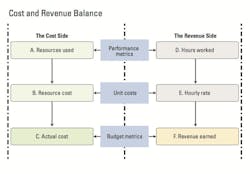

I use this diagram to unscramble situations and understand where the problem lies. Let’s first look at how we spend money: the cost side. Resources are used up as machines work (Block A), and resources cost money (Block B). These two numbers multiplied together give the actual cost (Block C). If a machine uses 120 gallons of fuel in a day and if fuel costs $3.65 per gallon, then the cost of fuel for the day is $438. If the machine has been on our books and working for six months, and if depreciation is $14,000 per month, then the depreciation charge will be $84,000. Various business systems capture and record the resources used, the unit cost of these resources, and the actual cost of owning and operating the machine; we need to code them and calculate them correctly.

Now, let’s look at how you balance your books and recover the costs experienced. Machines work to earn “revenue” or, more correctly, their earned value budget. They do this by working a certain number of hours (Block D) at a budgeted hourly rate (Block E). The revenue, or budget earned (Block F), is thus the product of the hourly rate and the hours worked. The earned-value budget concept means that machines are not given a budget to offset against their cost, they earn it at a given hourly rate for each hour they work. We go to a lot of trouble to set the hourly rate (See “Accomplish the Most Important Task,” June 2014), but all too frequently, the procedures we use for recording and validating hours worked receives little attention.

Nothing in the budgeting and cost-recovery system shown in the diagram will function if procedures are not in place to ensure that hours worked are recorded reliably and efficiently. The physical performance metrics such as gallons of fuel per hour and mechanic hours per operating hour will be distorted beyond value, the unit rates calculated will be meaningless, and the budget metrics used to measure performance will be wrong. In fact, if you get hours worked wrong, nothing in the equipment costing system works.

Five steps to ensure accurate recording of hours.

1. Keep it simple. We spend a lot of time recording hours worked for low-value units such as pumps and variable-message boards that stay on a given site for a long time. Develop simple daily or weekly reporting systems based on the date dispatch records for these types of units. Things add up, and too often small units go unreported for months at a time. This is especially true for units that have no operator with direct responsibility for reporting. Develop a simple system, attach units to individuals, and use payroll records to measure machine hours worked. Use default numbers and reduce daily pencil-and-paper reporting to the minimum.

2. Look to your culture. It is not smart to under-report hours to improve results or lower apparent job costs. It must not be part of the culture in your organization. Deliberately cutting hours worked in the misplaced belief that it is a victory in an arm wrestling match between operations and equipment should not be tolerated. Everyone needs to understand the importance of accurate, reliable information. Train, communicate and eliminate it from the system.

3. Check every unit. Do you know where every unit is? Is someone recording its location on a job site or in the yard? Have some units that should be earning revenue simply gone off the radar screen? You cannot have units—either idle or working—that are not reported. Worst of all, you cannot have working units go unaccounted for. Every unit on the fleet register must be visible. There has to be a revenue for every unit that experiences cost.

4. Validate reported hours. There are many ways to record hours worked. Service meter hours, time cards, and daily reports will give results that differ slightly. Decide how you are going to define hours worked and use other closely related metrics to check and validate. It is fine to use reported hours for charging sites and service meter hours for the PM program. But there should be a relationship. Know the relationship, check and validate. Be aware of discrepancies.

5. Use technology. Many state-of-the-art fuel inventory systems enable reliable and accurate recording of hours worked as part of the fueling process. This is helpful, and the information produced can be used to check and validate daily reports. In addition, we are all looking forward to the day when machines report for themselves and by themselves and when we can obsolete many of our pencil-and-paper systems. There remain problems to be solved (see “The Quality of the Data,” September 2014 ), but the day is not far off when all we will need to do is code hours worked to job phases. This will bring about major changes and will give us yet another, and perhaps more reliable, metric for hours worked.

We have so far focused on the role of hours worked in equipment costing. It is critical to realize that this is not the only part of our business that relies on this metric. Our PM system, our utilization calculations, fuel burn calculations, age, and component-replacement calculations all rely on hours worked. The same is true for our job costing, productivity measurement, and bidding. Indeed, it is difficult to think about a single part of the company that is not affected by hours worked. So, if you get it wrong, you start a cancer that spreads to every part of the company. All management data becomes suspect, and you lose the ability to make good decisions at the right time. Hours worked is truly at the core of our information system.

It is difficult to run a store and set the price for a can of peas if you do not know how many cans you have sold. You may know what you have spent to the cent, but to get it right you absolutely have to know how many cans have been sold. It is the same with hours worked. It is a critical number. Getting it right makes your whole system work.